Petrochemical Feedstock Vulnerability and the M&A Response

Problem, Actual Deal Flow, and Forward Opportunities: April 2026

Part 1 — The Industrial Problem

The European and Asian petrochemical industries sit on a structurally exposed feedstock base. Roughly 83% of global naphtha is derived from crude oil [1], European crackers are historically ~78% naphtha-dependent [2], and Asia-Pacific consumes 44% of global naphtha [3]. When Brent sustains prices above roughly $95/bbl, commodity polymer producers can typically pass through only 60–70% of the cost increase, and pass-through breaks down entirely when feedstock costs rise more than ~30% over a six-month window. The 2026 Iran conflict — with the Strait of Hormuz effectively closed from early March [4] — has pushed European naphtha crackers past that line. The carbon overhead compounds the pain: EU ETS costs plus the phasing-in of the Carbon Border Adjustment Mechanism add roughly $80–110 per ton of ethylene for European producers, a structural cost that did not exist in prior oil shocks and does not disappear when crude normalizes.

The shock is landing on an industry already in active rationalization. European ethylene operating rates were running 70–75% in mid-2025, well below the 80–90% viability threshold [5]; European chemical plant closures have grown sixfold since 2022, with 17.2 million tons of capacity announced for closure in 2025 alone and investment in new European capacity down 86% [6]; and roughly 21 million tons of global ethylene capacity is expected to shut by 2028 [7]. Downstream, the cascade extends into packaging, automotive (already in structural decline in Europe), and agriculture — Gulf-region urea prices rose roughly 50% in the first month of the conflict [4]. Industry analysts have converged on M&A as the strategic response of choice — acquisition of European brownfields, waste infrastructure, circular pure-plays, bio-naphtha specialists, and integrated circular refineries. The transaction record over 2024 to early 2026 tells a different story.

Part 2 — The Actual Deal Flow, 2024–2026

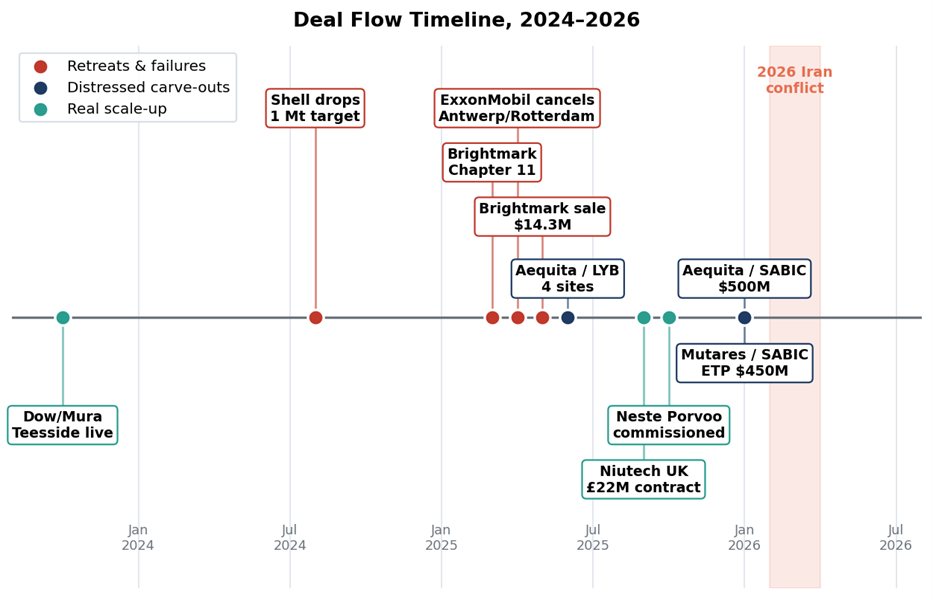

The M&A activity actually closing in the market is not a chemical-major roll-up of circular assets. It is a wave of distressed carve-outs to specialist private equity, parallel retreats by chemical majors from earlier circular commitments, and a small number of incremental scale-up moves by a different set of players than the strategic literature predicted.

Figure 1. Deal flow timeline, 2024–2026. Three parallel stories: chemical-major retreats, distressed PE carve-outs, and incremental scale-up.

2.1 Aequita privatizes European petrochemicals

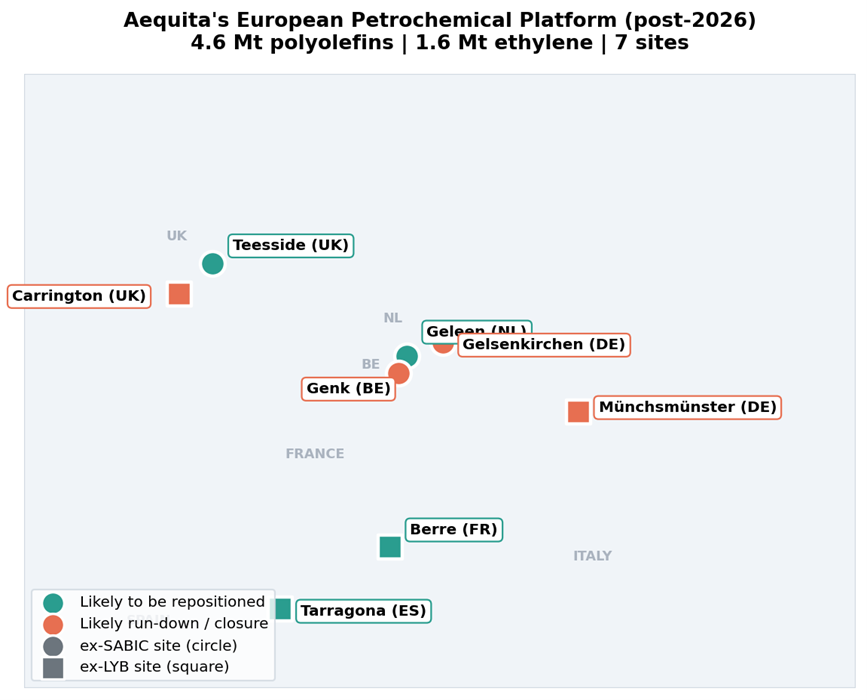

The most significant European petrochemical story of the period is a Munich-based private equity firm, Aequita SE & Co. KGaA, becoming Europe’s largest polyolefins producer in eight months. In June 2025, Aequita entered exclusive negotiations to acquire four LyondellBasell European sites: Berre, Münchsmünster, Carrington, and Tarragona [8]. The deal structure is striking: LyondellBasell contributed €265 million in cash versus only €10 million from Aequita [9]. The seller paid the buyer to take the assets. As a direct result, LYB’s capacity share in cost-advantaged regions (US and Middle East) rises from 61% to 68% [9].

Seven months later, in January 2026, Aequita signed a further agreement to acquire SABIC’s entire European Petrochemicals business — Geleen, Teesside, Gelsenkirchen, and Genk — for an enterprise value of $500 million [10][11]. SABIC’s announcement stated explicitly that the consideration would be “settled entirely via two perpetual vendor notes repayable based on future cashflows” [11] — near-zero upfront cost. SABIC took a non-cash writedown of approximately $2.88 billion [12]. Combined, the two acquisitions make Aequita Europe’s largest polyolefins producer with 4.6 million tonnes of capacity across seven sites, with combined revenues approaching $7 billion [13].

A parallel transaction the same day saw another German PE firm, Mutares, acquire SABIC’s Engineering Thermoplastics business in the Americas and Europe for an implied value of $450 million, also with minimal upfront [7].

Figure 2. Aequita’s European platform post-2026. Geographic dispersion shapes which sites are likely to be repositioned as circular refineries (coastal, integrated, circular-anchored) and which will be run down.

These are not strategic acquisitions by chemical majors responding to the Iran conflict. They are financial carve-outs that allow former owners to deconsolidate loss-making operations while specialist industrial PE firms attempt to extract synergies. Wood Mackenzie described Aequita’s position as a bet on a “European chemicals renaissance,” with the thesis dependent on cost-out and consolidation rather than on competitive feedstock economics.

2.2 The quiet retreat from chemical recycling

The circular feedstock picture is not the roll-up story either. In July 2024, Shell abandoned its goal of recycling 1 million tonnes of plastic waste into pyrolysis oil by 2025, citing slow technology development, feedstock shortages, and regulatory uncertainty [14]. ExxonMobil halted approximately €100 million of pyrolysis investments in Antwerp and Rotterdam in 2025 [15], though it completed a smaller 30,000-tonne captive facility at Baytown, Texas [16]. Encina cancelled its planned $1.1 billion pyrolysis facility in Point Township, Pennsylvania [17].

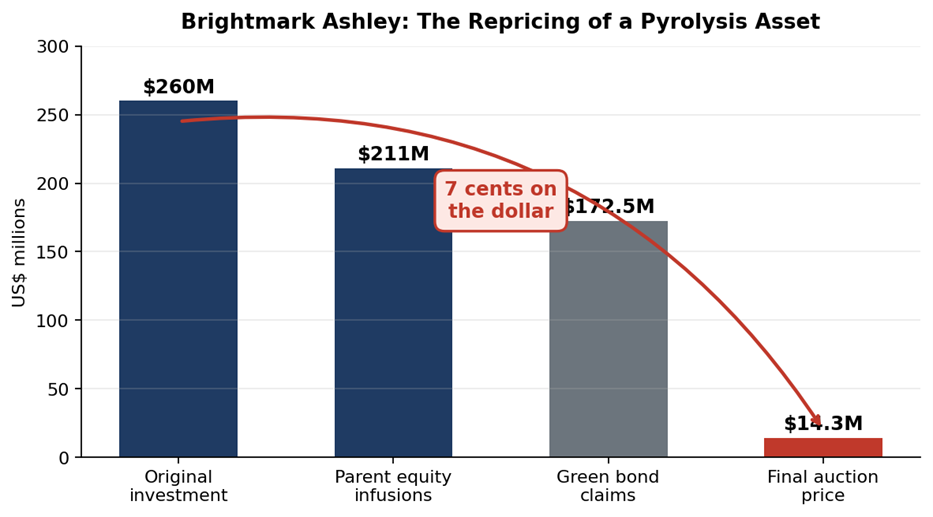

The most instructive failure is Brightmark’s. In March 2025, Brightmark’s subsidiaries operating its flagship Ashley, Indiana pyrolysis plant filed for Chapter 11 after defaulting on a $12.9 million payment on $172.5 million of green bonds [18]. The facility was originally a $260 million Circularity Center designed to process 100,000 tonnes/year. By the time of bankruptcy, it was operating at 5% of nameplate capacity despite over $211 million in parent equity infusions [19].

Figure 3. The Brightmark repricing. A marketed sale process that contacted 332 parties and drew 4 qualified bidders produced a final price of 7% of original cost [19][20].

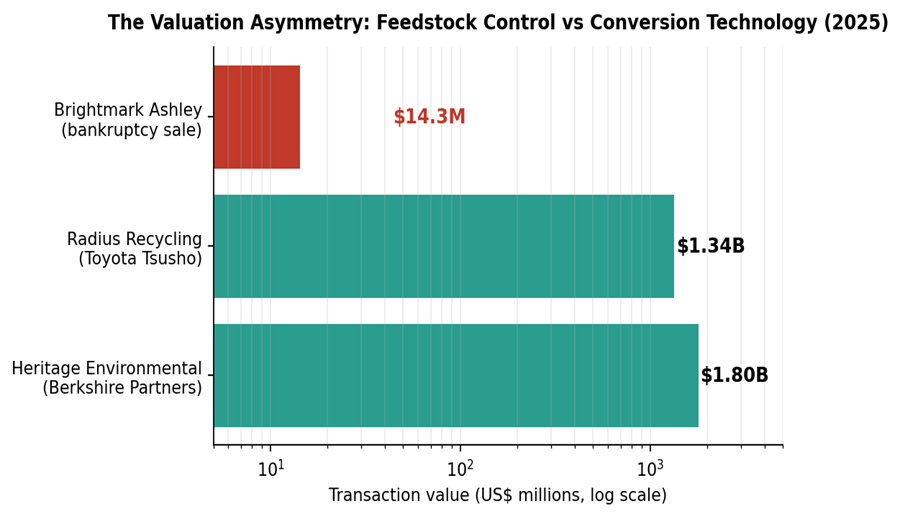

Through a 26-round auction that drew four qualified bidders (UMB Bank, Freepoint Eco-Systems, Braven Environmental, and the parent), Brightmark LLC reacquired the facility for $14.3 million in cash [19] — roughly 7% of the original investment, or 8 cents on the dollar against bond claims. 332 parties had been contacted by the bankers; 24 signed NDAs [20]. The robust marketing process produced four real bids, and the highest cash offer was less than 8% of the cost basis. This is the new market price for a commercial pyrolysis plant.

2.3 What is genuinely scaling up

Several genuinely strategic deployments are in progress, but at smaller scale than the conventional thesis predicted. Dow and Mura Technology opened the world’s first commercial-scale HydroPRS plant at Teesside in October 2023 and plan to add up to 600 kilotons of capacity by 2030 through multiple facilities [21]. Dow has separately made minority investments in Xycle (21 kt Rotterdam) and Plastogaz [21].

Neste commissioned the world’s largest upgrading facility for liquefied waste plastic at Porvoo, Finland at end-2025 [22]. Neste’s 2025 revenue was €19.0 billion and its renewables capacity is expected to reach 6.8 million tonnes per year by 2027 — making Neste, not any traditional petrochemical major, the largest single player in alternative feedstocks. Honeywell UOP has built its business on licensing plus JVs (Sacyr in Spain, Avangard Innovative in Texas, licensing deals in China and Turkey) at a standard 30,000 tpa plant scale — the “sweet spot” for feedstock that can be gathered in a midsize city [16].

The most notable Middle Eastern circular deployment is happening at home, not abroad. Aramco, TotalEnergies, and SABIC have produced ISCC+ certified circular polymers at the SATORP refinery in Jubail, Saudi Arabia, with SABIC affiliate PETROKEMYA as offtaker [23]. This is the operating example that most closely matches the integrated circular refinery vision — but built domestically in Saudi Arabia rather than acquired in Europe. Separately, Chinese pyrolysis equipment firm Niutech signed a £22 million contract to deliver a 60,000-tpa production line to a UK client in late 2025 [24], a new competitive dynamic that reduces the strategic value of acquiring Western technology pure-plays.

2.4 Summary of documented transactions

| Date | Buyer / Seller | Asset | Value | Type |

| Jun 2025 | Aequita / LyondellBasell | 4 EU sites (Berre, Münchsmünster, Carrington, Tarragona) | LYB contributes €265M; Aequita €10M | Distressed carve-out |

| Jan 2026 | Aequita / SABIC | SABIC Europe (Geleen, Teesside, Gelsenkirchen, Genk) | $500M EV via vendor notes; $2.88B writedown | Distressed carve-out |

| Jan 2026 | Mutares / SABIC | ETP business (Americas & Europe) | $450M implied; minimal upfront | Distressed carve-out |

| Mar–May 2025 | Brightmark / Brightmark Indiana | Ashley, IN pyrolysis plant (originally $260M) | $14.3M cash (Ch. 11 363 sale) | Bankruptcy auction |

| 2025 | ExxonMobil | Antwerp & Rotterdam pyrolysis | ~€100M cancelled | Project cancellation |

| Jul 2024 | Shell | 1 Mt/yr pyrolysis target | Dropped | Strategic retreat |

| Apr 2024 | Encina | Point Township, PA ($1.1B planned) | Cancelled | Project cancellation |

| Oct 2023 | Dow / Mura Technology | Teesside HydroPRS; 600 kt target by 2030 | Undisclosed | Strategic JV |

| Late 2025 | Neste (organic) | Porvoo pyrolysis oil upgrader | Internal capex | Organic build |

| 2023+ | Aramco/TotalEnergies/SABIC | SATORP/PETROKEMYA ISCC+ polymer (Saudi Arabia) | Internal | Domestic integration |

| Sep 2025 | Niutech / UK client | 60 kt/yr pyrolysis equipment | £22M | Equipment supply |

| 2025 | Berkshire Partners / Heritage Environmental | US environmental services platform | $1.8B | PE platform deal |

| 2025 | Toyota Tsusho / Radius Recycling | US metals recycling | ~€1.34B | Strategic acquisition |

Figure 4. The valuation asymmetry. Waste and feedstock platforms attract billion-dollar transactions; pure-play chemical recycling assets clear at bankruptcy prices. The market is pricing feedstock control, not conversion technology.

Two patterns are clear. First, the largest petrochemical transactions of the period are distressed carve-outs to PE firms, not strategic acquisitions by chemical majors. Second, the chemical recycling sub-sector is producing project cancellations and bankruptcy sales rather than strategic acquisitions, while the few closed deals (Dow/Mura, Dow/Xycle, Honeywell UOP JVs) are all at the 20–60 kt scale rather than the headline 100–450 kt plants announced in 2021–2022.

Part 3 — Forward M&A Opportunities, 12–24 Months

The near-term opportunities cluster around six themes. Each is grounded in a specific observable condition in the current market.

3.1 Aequita follow-on transactions

Aequita now controls 4.6 million tons of European polyolefins capacity across seven sites but has neither the technology nor the institutional mandate to be a long-term integrated petrochemical operator. Aequita’s typical hold period runs 5–7 years, which implies one or more sites will likely come back to the market within that window — either as bolt-on transactions to other PE platforms or as strategic re-acquisitions at depressed valuations.

The site-by-site assessment shown in Figure 2 points to the likely repositioning candidates: Geleen (Plastic Energy SPEAR JV infrastructure already on site), Teesside (adjacent to Dow/Mura HydroPRS), Berre (coastal French Mediterranean access), and Tarragona (port access and downstream flexibility). The likely run-down candidates: Carrington and Münchsmünster (smaller, older, no circular anchor), Gelsenkirchen and Genk (structural cost disadvantage with no clear turnaround path). A researcher should track Aequita’s operational improvements quarterly and watch for re-marketing signals from mid-2027 onward.

3.2 Distressed pyrolysis asset acquisition

The Brightmark Indiana auction established a market-tested floor for distressed pyrolysis assets at roughly 7% of construction cost. Building a commercial pyrolysis plant organically takes 5–7 years; buying a failed plant at bankruptcy prices and fixing it can compress that timeline to roughly 18 months. For a strategic acquirer with genuine engineering capability to run a plant at nameplate capacity — a capability the original developers conspicuously lacked — assets are now available at single-digit cents on the dollar. The 24 NDAs signed in the Brightmark auction represent a self-identified universe of distressed-asset buyers.

Realistic near-term targets: Brightmark’s Thomaston, Georgia project if it enters distress (currently in air-permit phase, but the $950 million planned cost looks ambitious against the Ashley cost discovery); any Encina facility if the company re-emerges with revised plans; and the broader European pyrolysis pipeline, where several mid-scale facilities are in various stages of financial stress. The rule of thumb emerging from Brightmark: assume 5–10x cost reduction from announced project value, and budget for significant commissioning work to reach nameplate.

3.3 Pyrolysis equipment OEM acquisition

The Niutech UK contract points to an overlooked category: pyrolysis equipment OEMs. As pure-play developers fail and project capital dries up, surviving equipment suppliers become more strategically valuable than the operators they supply. Equipment OEMs offer simpler unit economics, less feedstock risk, and leverage to any operational recovery. Realistic acquirers are engineering firms (Technip Energies, KBR, Wood) rather than chemical majors.

3.4 Waste-stream platform consolidation

The asymmetry shown in Figure 4 is the strategic signal. Feedstock control is the binding constraint, and the market is pricing it accordingly. The practical opportunity is to acquire a sorted-stream waste platform first and a conversion technology second — the inverse of the sequencing chemical majors attempted in 2021–2022. A pyrolysis plant without a steady, sorted, contamination-controlled waste stream is a stranded asset, and whoever signs the regional waste aggregator to an exclusive contract determines who runs the conversion plant.

Realistic targets sit below the tier-one level. The tier-one waste operators — Veolia and Suez in Europe; Waste Management, Republic Services, GFL Environmental, and Casella in North America — are too large and too municipal-focused for clean acquisition. Berkshire Partners’ $1.8 billion acquisition of Heritage Environmental in early 2025 [25] signalled the floor price for a tier-one-adjacent platform. The specific targets worth screening are regional sorting and materials recovery facility operators in Germany, the Netherlands, and Belgium (near the Aequita-controlled petrochemical footprint), and their equivalents in the US Southeast and Midwest (near Brightmark’s Thomaston project and similar emerging plants). The practical structure is either a minority equity stake combined with an exclusive long-term offtake contract for sorted plastic streams, or outright acquisition of a dedicated sorting subsidiary. Valuations in this space have not yet moved substantially — a temporary condition.

3.5 Joint development agreements into Gulf complexes

The Aramco/TotalEnergies/SABIC SATORP deployment is the only operating example of an integrated circular value chain in a low-cost-energy region. If this model proves out at commercial scale over 2026–2027, the next wave of deals will be joint development agreements and equipment licensing into other Gulf petrochemical complexes — particularly ADNOC (Ruwais) and QatarEnergy (Ras Laffan).

The working deal templates are already established. The co-located feeder JV places a pyrolysis plant on or adjacent to an existing cracker site to supply pyrolysis oil as a virgin naphtha co-feed — SABIC’s joint venture with Plastic Energy at Geleen (SPEAR — SABIC Plastic Energy Advanced Recycling) is the template. The minority-plus-offtake structure involves 15–25% equity in a pure-play in exchange for exclusive long-term offtake — BASF’s earlier €20 million stake in Quantafuel and Dow’s pyrolysis-oil supply agreement with Fuenix Ecogy both follow this logic. For Western technology holders (Plastic Energy, Mura Technology, Eastman, Carbios), Gulf JVs are the most attractive realistic exit route. The acquirer pattern to watch: Middle Eastern state-backed producers taking minority stakes in Western pure-plays in exchange for exclusive deployment rights within the Gulf region.

3.6 Bio-naphtha and PET depolymerization

Neste’s scale and integration advantages have effectively closed the top of the bio-naphtha market to new entrants via organic build-out. The M&A opportunities are below Neste-scale: tall-oil and waste-oil aggregators, pre-upgrader bio-refineries, and specialist bio-naphtha producers serving regional markets. UPM Biofuels (tall-oil-based BioVerno line) is the most prominent European specialist. Smaller targets exist in waste cooking oil aggregation across Southern Europe and in second-generation biofuel plants that could pivot to bio-naphtha production.

PET depolymerization is a distinct play. It is narrower in addressable market than pyrolysis, but produces virgin-grade monomer and is the only realistic pathway to food-contact recycled content under EU Packaging and Packaging Waste Regulation rules. The credible European targets are Carbios (France, enzymatic depolymerization, strongest IP moat and food-contact certification path) and Loop Industries (Canada, with Suez European partnership via glycolysis). Eastman’s methanolysis platform at Kingsport is at commercial scale but accessible only via licensing or JV rather than acquisition. Indicative deal sizes run €300–700 million per specialist.

The risk in bio-naphtha is feedstock competition: it competes with renewable diesel and sustainable aviation fuel for the same molecules, and SAF mandates in Europe and North America create a structural pricing floor that tightens acquisition economics. For acquirers who can tie bio-naphtha supply directly into an existing polymer complex through a long-term offtake arrangement, the economics improve substantially.

Conclusion

The gap between what industry strategy literature has proposed since 2022 — aggressive strategic acquisition of European brownfields and circular pure-plays by chemical majors — and what is actually closing in the market reflects the fact that chemical majors have concluded, correctly or not, that European petrochemical operations cannot be rescued through incremental circular investment, and that the economics of standalone chemical recycling have not yet justified the capital the thesis requires. European brownfields are going to German PE at near-zero upfront cost. Chemical recycling pure-plays are going through bankruptcies at 7 cents on the dollar. The only integrated circular deployment is in Saudi Arabia.

Against that backdrop, the opportunities over the next 12 to 24 months are concrete and grounded in observable transactions: follow-on transactions on Aequita-held assets as the PE owner repositions or exits; distressed pyrolysis purchases at repriced valuations; equipment OEM consolidation; sorted-waste platform acquisitions below tier-one; joint development agreements into Gulf complexes; and bio-naphtha aggregator and PET depolymerization roll-ups below Neste scale. None of these are the headline strategic acquisitions imagined in earlier industry forecasts. All of them are accessible to a disciplined researcher with realistic valuation expectations.

References

All sources accessed April 2026.

[1] Market.us. Naphtha Market — petrochemical feedstock 63.2% share; crude oil 83.2% of naphtha source (2024). https://market.us/report/naphtha-market/

[2] Statista / Deloitte. Feedstock mix of petrochemicals by world region — Europe 78% naphtha (2017). https://www.statista.com/statistics/1108151/global-petrochemicals-feedstock-mix-by-region/

[3] Data Bridge Market Research. Global Naphtha Market — Asia-Pacific 44.3% share, 2024. https://www.databridgemarketresearch.com/reports/global-naphtha-market

[4] Wikipedia contributors. 2026 Strait of Hormuz crisis — closure dynamics, urea price +50%. https://en.wikipedia.org/wiki/2026_Strait_of_Hormuz_crisis

[5] SunSirs. European Chemical Plant Closures — ethylene operating rates 70–75% mid-2025. https://www.sunsirs.com/commodity-news/petail-26916.html

[6] CEFIC / Roland Berger (via CHEManager). Europe’s Chemical Sector Under Stress — 17.2 Mt 2025 closures; 86% drop in investment. https://chemanager-online.com/en/news/europes-chemical-sector-under-stress

[7] Chemical & Engineering News. Sabic to sell US, European assets on the cheap — combined platform revenues; Mutares ETP deal. https://cen.acs.org/business/petrochemicals/SABIC-sell-US-European-assets/104/web/2026/01

[8] LyondellBasell. LyondellBasell enters into an agreement and exclusive negotiations with AEQUITA — June 5, 2025. https://www.lyondellbasell.com/en/who-we-are/updates-events/corporate–financial-news/lyondellbasell-enters-into-an-agreement-and-exclusive-negotiations-with-aequita-for-the-sale-of-four-european-strategic-assessment-assets/

[9] LyondellBasell SEC filing / investor presentation. European Asset Sale, June 5, 2025 — LYB contributes €265M, Aequita €10M; cost-advantaged capacity 61% → 68%. https://s204.q4cdn.com/455115734/files/doc_downloads/2025/06/05/LYB-European-Asset-Sale.pdf

[10] Chemistry World. Sabic offloads petrochemicals and plastics plants — Aequita $500M for Teesside, Geleen, Gelsenkirchen, Genk. https://www.chemistryworld.com/news/sabic-offloads-petrochemicals-and-plastics-plants-in-europe-and-americas/4022818.article

[11] Saudi Stock Exchange (Tadawul). SABIC announcement of AEQUITA agreement — January 7, 2026; perpetual vendor notes. https://www.saudiexchange.sa/wps/portal/saudiexchange/newsandreports/issuer-news/issuer-announcements/issuer-announcements-details/?anId=92518&anCat=1&cs=2010&locale=en

[12] Argus Media. Sabic to sell European business to Aequita — $500M, $2.88B writedown; Geleen capacity. https://www.argusmedia.com/en/news-and-insights/latest-market-news/2773318-sabic-to-sell-european-business-to-aequita-update

[13] Wood Mackenzie. Is AEQUITA placing a risky bet on a European chemicals renaissance? — 4.6 Mt polyolefins / 1.6 Mt ethylene. https://www.woodmac.com/news/opinion/aequitas-european-experiment/

[14] IDTechEx. Shell’s Move Leads to Speculation of the Future of Pyrolysis — 1 Mt target dropped July 2024. https://www.idtechex.com/en/research-article/shells-move-leads-to-speculation-of-the-future-of-pyrolysis/31811

[15] Recycling International. Recap: What happened on the recycling stage in 2025 — ExxonMobil halts ~€100M Antwerp/Rotterdam. https://recyclinginternational.com/commodities/recap-what-happened-on-the-recycling-stage-in-2025/62819/

[16] Chemical & Engineering News. Amid controversy, chemical companies bet on plastics pyrolysis — Honeywell UOP JVs; ExxonMobil Baytown. https://cen.acs.org/environment/recycling/Amid-controversy-industry-goes-plastics-pyrolysis/100/i36

[17] Waste Dive. Chemical recycling updates from Brightmark, Encina and ExxonMobil — Encina Pennsylvania cancellation. https://www.wastedive.com/news/chemical-recycling-brightmark-encina-exxonmobil-plastic/714156/

[18] Chemanalyst. Brightmark’s Subsidiaries Declare Bankruptcy — March 2025; $172.5M green bonds; 5% capacity. https://www.chemanalyst.com/NewsAndDeals/NewsDetails/brightmark-subsidiaries-declare-bankruptcy-amid-chemical-recycling-debt-crisis-35240

[19] Elevenflo. Brightmark Plastics: $260M Facility Sells for $14M — 26-round auction; 7% of cost basis. https://elevenflo.com/blog/brightmark-plastics-chapter-11-bankruptcy

[20] Resource Recycling. Brightmark Indiana auction advances post-bankruptcy — 332 parties contacted, 24 NDAs. https://resource-recycling.com/plastics/2025/04/16/brightmark-indiana-auction-advances-post-bankruptcy/

[21] Dow Inc.. Advanced Recycling Systems — Mura Technology HydroPRS Teesside; 600 kt target by 2030; Xycle Rotterdam. https://www.dow.com/en-us/materials-ecosystem/advanced-recycling.html

[22] Neste. Neste commissions the world’s largest upgrading facility for liquefied waste plastic — Porvoo, late 2025. https://www.neste.com/news/neste-commissions-the-worlds-largest-upgrading-facility-for-liquefied-waste-plastic-and-scales-up-chemical-recycling

[23] Packaging Europe. Aramco, TotalEnergies and SABIC generate certified circular polymers — SATORP Jubail; PETROKEMYA; ISCC+. https://packagingeurope.com/news/aramco-totalenergies-and-sabic-generate-certified-circular-polymers-from-plastic-waste-derived-oil/10103.article

[24] Hydrocarbon Processing. Niutech 60 kt UK pyrolysis contract — £22M equipment supply, September 2025. https://www.hydrocarbonprocessing.com/news/2025/09/next-generation-pyrolysis-line-drives-global-chemical-recycling-of-waste-plastics/

[25] Waste Dive. 2025’s notable waste and recycling acquisitions — Berkshire Partners $1.8B Heritage Environmental. https://www.wastedive.com/news/2025-notable-waste-and-recycling-acquisitions/808593/

Methodology note.

Transactions documented in this paper are drawn from the cited sources: direct company announcements (LyondellBasell, SABIC, Neste, Dow), regulatory filings (Saudi Tadawul, US bankruptcy court documents), and trade press reporting (C&EN, ICIS, Chemical Week, Wood Mackenzie, Argus). Deal terms reflect public reporting as of the cited dates. The site-by-site repositioning assessment in Figure 2 and the forward opportunities in Part 3 are author observations based on the documented deal record.