Air Cargo Market Review: Not enough planes, not enough workers

From the Cognos Global Partners Transportation and Logistics Group

Air Cargo Market Review Part 1:

Not enough planes, not enough workers

Air cargo demand is set to grow faster than dedicated freighter capacity through the late 2020s, keeping freight markets relatively tight and supporting elevated yields in the near term, with gradual easing into the early–mid 2030s as Airbus and Boeing work through backlogs and restore higher production rates. Labour shortages in manufacturing and MRO will be a binding constraint over the next five years, magnifying these capacity limits and modestly reducing effective fleet growth versus what headline orderbooks suggest.

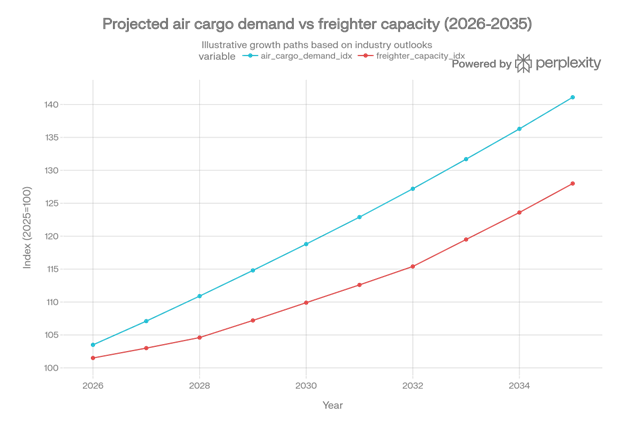

Air cargo demand versus capacity 2026–2035

Demand and capacity trajectory

Both Airbus and Boeing forecast world air cargo traffic growth around the mid‑3% CAGR range over the next 20 years, driven by e‑commerce, emerging market trade, and modal shift from ocean for some high‑value goods.

Freighter fleet growth is projected to be slower than traffic growth in the near term because many older freighters are being retired for cost and emissions reasons and conversion slots for passenger‑to‑freighter (P2F) aircraft are constrained.

The illustrative chart below shows demand and dedicated freighter capacity indexed to 2025 = 100, with demand growing at about 3.5% per year and capacity lagging in the late 2020s before gradually catching up in the 2030s:

| Year | Demand index (2025=100) | Freighter capacity index (2025=100) |

| 2026 | 103.5 | 101.5 |

| 2030 | 118.6 | 108.1 |

| 2035 | 141.0 | 125.9 |

This gap reflects that widebody passenger aircraft, which carry significant belly cargo, are also capacity‑constrained by long lead times and certification/production issues, limiting total system capacity even beyond pure freighters.

Airbus and Boeing production and backlogs

Narrowbody and widebody output

Airbus has stated medium‑term targets of about 75 A320‑family jets per month later this decade, with A350 production moving toward mid‑teens per month, but actual ramp‑up has been slower due to supply chain and labour constraints.

Boeing, after the 737 MAX and 787 production disruptions, is targeting a gradual climb toward 50+ 737s per month and higher 787 output, but near‑term caps from regulators and supplier quality issues are keeping realized rates below plan.

Backlogs and implications for cargo

Both OEMs carry record commercial backlogs, with thousands of narrowbodies and several hundred widebodies on order; freighter‑specific types (777F/777‑8F, A350F, 767F, A330P2F, 737/A321 P2F) make up a smaller but strategically important share.

Lead times for new‑build freighters are effectively stretching toward the early 2030s, and P2F conversion lines are largely sold out for several years, limiting how quickly the industry can respond to sustained demand spikes.

In practice, this means that even if demand surprises to the upside, incremental dedicated cargo capacity must come from higher load factors, better utilization, and opportunistic use of belly space, rather than a rapid influx of new metal.

Freight rate implications (short, mid, long term)

Short term (0–3 years)

- With demand outpacing dedicated capacity growth and limited elasticity in the passenger widebody fleet, structural load factors in key trade lanes should remain high compared to pre‑COVID levels.

- This supports freight rates staying above 2015–2019 averages, even though they are well below the extreme peaks seen during the pandemic and immediate aftermath.

Medium term (3–7 years)

- As Airbus and Boeing work through some of the widebody backlog and conversion capacity increments come online, the gap between demand and capacity narrows but does not fully close.

- Freight rates are likely to normalize further but remain cyclically supported, with less severe rate collapses during downturns because structural retirements and fleet age profiles keep a lid on oversupply.

Long term (7–10+ years)

- By the early‑mid 2030s, assuming OEMs achieve targeted production rates and conversion capacity expands, system capacity growth could come into closer alignment with traffic growth, easing structural tightness.

- In that environment, freight costs should trend closer to long‑run marginal cost, with greater sensitivity to fuel prices and environmental charges (CORSIA, ETS, SAF mandates) than to pure aircraft availability.

An illustrative example: if demand grows ~3.5% per year while capacity grows only ~2% for the next five years, average load factors might sit 3–5 percentage points above historical norms, supporting yields 10–20% above pre‑COVID baselines; by the 2030s, that premium could shrink into the single digits as more aircraft deliver.

Drivers of labour shortages (manufacturing and MRO only)

Structural and cyclical factors

- Demographics and retirements: a large cohort of experienced mechanics, engineers, and machinists is reaching retirement age, and replacement pipelines have lagged, especially in North America and Europe.

- Skills pipeline: STEM and skilled‑trades enrolment has not kept pace with demand, and competing sectors (tech, energy transition, advanced manufacturing) often offer more flexible conditions, drawing talent away from aerospace.

Sector‑specific constraints

- Regulatory and certification barriers: licensed aircraft maintenance technicians, avionics specialists, and airframe/engine overhaul staff must meet stringent regulatory requirements, making it slow and costly to add headcount.

- Post‑COVID volatility: the sharp demand collapse in 2020 followed by an unexpectedly fast rebound led to layoffs and early retirements, then rapid re‑hiring, but many experienced workers did not return, leaving a skills gap that persists.

Cybersecurity, digitalisation, and increased reliance on advanced materials and complex avionics also raise the skills bar for both new‑build assembly and MRO, lengthening training times and amplifying the shortage.

Quantitative impact on deliveries and in‑service availability

Production throughput

- OEMs and major tier‑1 suppliers report that labour and skills shortages are a top constraint on achieving planned rate increases, alongside engine availability and parts supply.

- Independent forecasts suggest that, relative to unconstrained plans, effective narrowbody and widebody output over the next 3–5 years could be 5–10% lower than originally targeted, with labour shortages responsible for a meaningful share of that delta.

For example, if a widebody line was planned to ramp from 7 to 12 aircraft per month by 2029 but only reaches 10 due to combined labour and supply constraints, that is roughly 24 fewer aircraft per year; if 25–30% of that shortfall is attributable to skilled labour scarcity, the labour component alone accounts for 6–8 aircraft per year not entering service.

MRO capacity and aircraft availability

- MRO providers project mid‑single‑digit annual growth in maintenance demand through 2035, but staffing levels are not keeping pace, leading to longer turnaround times (TAT) and higher shop visit backlogs.

- If average heavy‑check TAT for a widebody increases from, say, 45 days to 55–60 days because of labour constraints, that can reduce effective fleet availability by 1–2 percentage points for affected operators.

Over a global fleet of thousands of aircraft, a 1–2 percentage point reduction in availability equates to dozens of aircraft’s worth of lost annual flying capacity, effectively tightening supply even if the physical fleet count rises.

Net effect on cargo capacity

- Delayed deliveries, especially of widebodies and dedicated freighters, combined with longer MRO downtimes, temper the growth of both belly and maindeck capacity vs. what orderbooks imply.

- For air cargo, this means that even with moderate traffic growth, labour‑driven constraints in manufacturing and maintenance will help keep capacity utilization high, reinforcing upward pressure on freight yields in the near to medium term.

Overall, the interplay of strong demand, constrained OEM output, and persistent labour shortages in manufacturing and MRO suggests a structurally tighter air cargo market through at least the early 2030s, with only gradual normalisation of freight costs as capacity and workforce bottlenecks ease.

| Year | air_cargo_demand_idx | freighter_capacity_idx |

| 2026 | 103.5 | 101.5 |

| 2027 | 107.1 | 103.0 |

| 2028 | 110.9 | 104.6 |

| 2029 | 114.8 | 107.2 |

| 2030 | 118.8 | 109.9 |

| 2031 | 122.9 | 112.6 |

| 2032 | 127.2 | 115.4 |

| 2033 | 131.7 | 119.5 |

| 2034 | 136.3 | 123.6 |

| 2035 | 141.1 | 128.0 |

Check soon back for Part II: The Air Cargo Market & Implications for Corporate Strategy